Introduction: Why Saving Money Fast Matters in 2025

With inflation rates fluctuating and the cost of living continuing to rise in 2025, learning how to save money fast on a low income has become more critical than ever. Whether you're building an emergency fund, planning a dream vacation, or working toward financial independence, these 25 proven money-saving strategies will help you cut expenses, boost income, and accelerate your wealth-building journey.

According to NerdWallet's financial research, the average American household can save between $5,000 to $15,000 annually by implementing strategic spending cuts and smart financial habits. This comprehensive guide provides actionable tips that work for students, families, and anyone looking to improve their financial situation quickly.

💰 Calculate Your Savings Potential

Before diving into money-saving strategies, use our free financial calculators to understand your current situation:

Part 1: Foundation - Track, Plan, and Automate Your Savings

1. Track Every Dollar You Spend (The 30-Day Challenge)

Why it works: You can't manage what you don't measure. Tracking reveals hidden spending patterns that drain your budget.

How to implement:

- Use free apps like Mint, YNAB (You Need A Budget), or PocketGuard

- Categorize expenses: housing, food, transportation, entertainment, subscriptions

- Review weekly to identify spending leaks

The Consumer Financial Protection Bureau recommends tracking expenses for at least 30 days to identify patterns and make informed decisions about where to cut costs.

Real Example: Sarah from Texas tracked her spending for 30 days and discovered she was spending $347/month on food delivery services she didn't realize added up. By cutting this to once weekly, she saved $2,820 annually.

Pro Tip: Set up spending alerts when you exceed category budgets to stay accountable. Use our Paycheck Calculator to understand exactly how much you can allocate to each category.

2. Set SMART Savings Goals (Specific, Measurable, Achievable)

Why it works: Vague goals like "save more money" fail. Specific targets create motivation and accountability.

How to set effective goals:

- Emergency Fund: Save 3-6 months of expenses ($10,000-$20,000 for most households)

- Short-term: Vacation fund ($3,000 in 6 months = $500/month)

- Long-term: House down payment ($40,000 in 4 years = $833/month)

Real Example: The Martinez family wanted to save $15,000 for a down payment. They broke it into monthly milestones ($625/month) and automated transfers every payday. They reached their goal in 24 months.

Action Step: Write down 3 specific savings goals with deadlines and monthly targets today.

3. Automate Your Savings (Pay Yourself First Strategy)

Why it works: Automation removes willpower from the equation. Money saved before you see it never gets spent.

Best automation strategies:

- Set up automatic transfers on payday (even $50/week = $2,600/year)

- Use employer 401(k) contributions (especially if they match)

- Try micro-saving apps like Acorns or Digit that round up purchases

Real Example: James automated $200 biweekly transfers to a high-yield savings account. After one year, he had saved $5,200 without thinking about it, plus earned $156 in interest (3% APY).

Pro Tip: Increase automatic savings by 1% every quarter as your income grows.

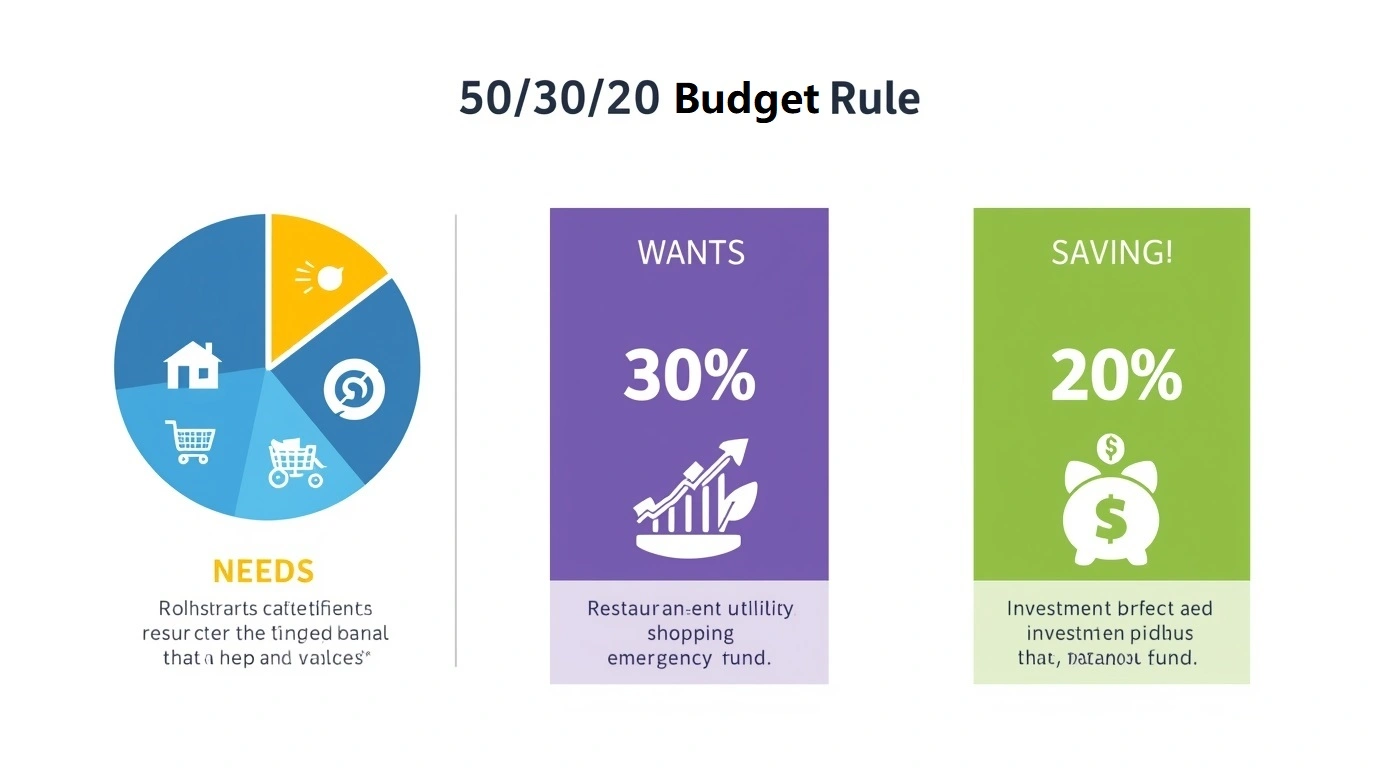

4. Use the 50/30/20 Budgeting Rule

Why it works: This simple framework prevents overspending while ensuring balanced financial health.

The breakdown:

- 50% - Needs (housing, utilities, groceries, insurance)

- 30% - Wants (dining out, entertainment, hobbies)

- 20% - Savings and debt repayment

This budgeting method, popularized by Senator Elizabeth Warren, is widely recommended by financial experts. Learn more about the 50/30/20 rule on Investopedia.

Real Example: On a $4,000 monthly income:

- Needs: $2,000

- Wants: $1,200

- Savings: $800 = $9,600 saved annually

Use our Salary Calculator to convert your hourly wage to monthly income and plan your 50/30/20 budget.

Adjustment for aggressive savers: Try 50/20/30 or even 50/10/40 to accelerate wealth building.

5. Open a High-Yield Savings Account (Earn While You Save)

Why it works: Traditional banks pay 0.01% interest. High-yield accounts pay 4-5% in 2025, earning you hundreds more.

According to Bankrate's latest survey, high-yield savings accounts are offering competitive rates in 2025, making them an essential tool for emergency funds.

Top options in 2025:

- Marcus by Goldman Sachs - 4.5% APY

- Ally Bank - 4.35% APY

- American Express Personal Savings - 4.3% APY

Real Example: $10,000 in a traditional bank earns $1/year. The same amount in a high-yield account at 4.5% earns $450/year - a $449 difference with zero effort.

Action Step: Transfer your emergency fund to a high-yield account this week.

Part 2: Cut Major Expenses (Save $500+ Monthly)

6. Negotiate Your Bills (Save $1,200+ Annually)

Why it works: Companies expect negotiation and often have retention departments authorized to offer discounts.

What to negotiate:

- Cable/Internet: Ask for promotional rates (save $30-50/month)

- Cell phone: Switch to prepaid plans (save $40-60/month)

- Insurance: Shop competitors annually (save $300-800/year)

- Credit card interest rates: Request APR reduction

The Federal Trade Commission provides guidance on negotiating with creditors and service providers to reduce your monthly expenses.

Real Example: Linda called her internet provider threatening to cancel. They immediately offered a $35/month discount for 12 months = $420 saved in a 15-minute call.

Script to use: "I've been a loyal customer for [X years], but I'm considering switching to [competitor] who offers [better rate]. Can you match or beat their offer?"

7. Cancel Unused Subscriptions (The $200/Month Leak)

Why it works: The average household has 12+ subscriptions, many forgotten or underused.

Common subscription traps:

- Streaming services ($15-20 each × 4 = $60-80/month)

- Gym memberships ($30-60/month, used 2× monthly)

- Software subscriptions ($10-30/month each)

- Magazine/news subscriptions ($5-15/month)

Real Example: The Johnson family audited subscriptions and found:

- Netflix, Hulu, Disney+, HBO Max ($68/month) - kept Netflix only

- Gym membership ($45/month) - switched to home workouts

- Unused app subscriptions ($23/month)

- Total saved: $136/month = $1,632/year

Action Step: Use Truebill or Rocket Money to identify and cancel subscriptions automatically.

8. Refinance High-Interest Debt (Save Thousands in Interest)

Why it works: Lowering interest rates means more money goes to principal, accelerating debt payoff.

Strategies:

- Credit card balance transfers: 0% APR for 12-18 months (save 15-25% interest)

- Personal loan consolidation: Combine multiple debts at lower rate

- Mortgage refinancing: Even 0.5% reduction saves thousands

If you're considering refinancing your mortgage, use our Mortgage Calculator Guide to determine if refinancing makes financial sense for your situation.

Real Example: Marcus had $15,000 in credit card debt at 22% APR ($3,300/year in interest). He transferred to a 0% APR card for 18 months and paid $833/month, saving $2,475 in interest and becoming debt-free faster.

Warning: Only refinance if you commit to not accumulating new debt.

9. Downsize Your Housing (The Biggest Expense)

Why it works: Housing typically consumes 30-40% of income. Reducing this creates massive savings.

Options:

- Get a roommate: Cut rent/mortgage by 30-50%

- Move to lower cost area: Save $300-800/month

- Downsize: Smaller home = lower mortgage, utilities, maintenance

- House hacking: Rent out spare room on Airbnb

Real Example: Kevin moved from a $1,800 studio to a $1,200 shared apartment with a roommate (his share: $600/month). Annual savings: $14,400 - enough for a house down payment in 3 years.

Alternative: If moving isn't possible, negotiate rent renewal or refinance your mortgage.

10. Drive a Reliable Used Car (Not a Depreciating Asset)

Why it works: New cars lose 20-30% value in year one. Used cars (3-5 years old) offer reliability without depreciation hit.

Smart car strategies:

- Buy certified pre-owned (CPO) with warranty

- Keep cars 10+ years to maximize value

- Pay cash or finance under 3 years

- Avoid luxury brands (higher maintenance)

Real Example: Instead of buying a $35,000 new SUV ($600/month payment), Rachel bought a 4-year-old certified Honda CR-V for $18,000 ($320/month). She saved $280/month = $3,360/year, plus lower insurance and registration fees.

Total 5-year savings: Over $20,000 compared to new car purchase.

Part 3: Reduce Daily Expenses (Small Changes, Big Impact)

11. Master Meal Planning (Save $400+ Monthly on Food)

Why it works: Meal planning eliminates food waste, reduces impulse purchases, and cuts restaurant spending.

The USDA's MyPlate offers free meal planning resources and budgeting tips to help families eat healthy while saving money.

The system:

- Plan weekly menus every Sunday

- Shop with a list (never hungry)

- Batch cook on weekends

- Use leftovers strategically

Real Example: The Chen family spent $1,200/month on food (groceries + dining out). After implementing meal planning:

- Groceries: $600/month (strategic shopping)

- Dining out: $200/month (reduced from $500)

- Total saved: $400/month = $4,800/year

Money-saving meal tips:

- Buy generic brands (save 30-40%)

- Shop seasonal produce

- Use cashback apps (Ibotta, Fetch Rewards)

- Cook double portions and freeze

12. Pack Your Lunch (The $2,500 Annual Savings)

Why it works: Restaurant lunches cost $10-15 daily. Homemade lunches cost $2-4.

The math:

- Restaurant lunch: $12 × 5 days × 50 weeks = $3,000/year

- Packed lunch: $3 × 5 days × 50 weeks = $750/year

- Savings: $2,250/year

Real Example: David started meal-prepping Sunday evenings: grilled chicken, rice, vegetables in containers. Cost per lunch: $3.50. He saved $2,125 annually and lost 15 pounds from healthier eating.

Easy lunch ideas:

- Mason jar salads

- Burrito bowls

- Pasta with protein

- Soup in thermoses

13. Brew Coffee at Home (The $1,000 Latte Factor)

Why it works: Daily coffee visits seem small but compound dramatically.

The calculation:

- Starbucks daily: $5 × 365 days = $1,825/year

- Home brewing: $0.50 × 365 days = $182.50/year

- Savings: $1,642.50/year

Real Example: Emma bought a $30 French press and quality beans ($12/bag, lasts 2 weeks). Her annual coffee cost dropped from $1,800 to $312, saving $1,488 - enough for a weekend vacation.

Compromise: Limit coffee shops to 2× weekly (save $1,300/year while keeping the treat).

14. Use the 30-Day Rule for Purchases (Eliminate Impulse Buying)

Why it works: Waiting 30 days eliminates emotional purchases. Most "must-haves" lose appeal.

How it works:

- See something you want to buy (non-essential)

- Add to a "30-day list" with date and price

- Wait 30 days

- If you still want it and can afford it, buy it

Real Example: Tom implemented the 30-day rule for purchases over $50. In 6 months:

- 12 items added to list

- 9 items no longer wanted after 30 days

- 3 items purchased (truly needed)

- Saved: $847 on impulse purchases

Psychology: This creates a cooling-off period that defeats marketing manipulation.

15. Shop with Cash (The Envelope System)

Why it works: Physical cash creates psychological pain when spending. Cards feel abstract.

The envelope method:

- Withdraw weekly cash for variable expenses

- Divide into envelopes: groceries, entertainment, dining out

- When envelope is empty, stop spending in that category

Real Example: The Williams family struggled with overspending. They switched to cash envelopes:

- Groceries: $150/week

- Entertainment: $100/week

- Dining: $75/week

- Result: Stayed within budget 90% of weeks, saving $350/month = $4,200/year

Modern alternative: Use debit cards with category spending limits.

Part 4: Increase Your Income (Earn More to Save More)

16. Start a Side Hustle (Extra $500-2,000 Monthly)

Why it works: Cutting expenses has limits. Income has no ceiling.

Top side hustles for 2025:

- Freelancing: Writing, design, coding ($25-100/hour)

- Rideshare/Delivery: Uber, DoorDash ($15-25/hour)

- Online tutoring: VIPKid, Tutor.com ($18-30/hour)

- Virtual assistant: $20-40/hour

- Selling digital products: Courses, templates, ebooks

Interested in content creation as a side hustle? Check out our YouTube Money Calculator Guide to estimate potential earnings from video content.

Real Example: Jessica started freelance writing 10 hours/week at $40/hour. Monthly income: $1,600. She saved 75% ($1,200/month) = $14,400/year toward her house fund.

Action Step: Identify one skill you can monetize this month.

17. Negotiate a Raise (Increase Your Primary Income)

Why it works: A $5,000 raise equals $416/month in extra savings potential.

How to negotiate effectively:

- Research market rates (Glassdoor, PayScale)

- Document your achievements and value

- Schedule formal meeting with manager

- Ask for specific amount with justification

Use the Bureau of Labor Statistics Occupational Employment and Wage Statistics to research average salaries in your field and location.

Before negotiating, use our Salary to Hourly Calculator to understand your true hourly worth and calculate the impact of a raise.

Real Example: After 2 years without a raise, Michael researched that his role paid $8,000 more at competitors. He presented his case with metrics showing he exceeded goals by 30%. Result: $6,500 raise = $542/month extra to save.

Timing: Best times to ask: after major achievement, during review cycles, or when taking on new responsibilities.

18. Sell Unused Items (Quick $1,000-5,000)

Why it works: The average home has $3,000+ in unused items gathering dust.

What to sell:

- Electronics (old phones, tablets, laptops)

- Furniture you don't use

- Clothes (Poshmark, ThredUp)

- Collectibles, books, DVDs

- Exercise equipment

Real Example: The Anderson family decluttered and sold:

- Old iPhone and iPad: $450

- Unused furniture: $680

- Clothes and shoes: $320

- Exercise bike: $200

- Books and DVDs: $150

- Total: $1,800 in one month

Best platforms: Facebook Marketplace, OfferUp, eBay, Poshmark, Mercari

19. Rent Out Assets (Passive Income Streams)

Why it works: Assets sitting idle can generate income without active work.

What to rent:

- Spare room: Airbnb ($500-1,500/month)

- Parking space: $100-300/month in cities

- Car: Turo ($300-800/month)

- Storage space: Neighbor.com ($50-200/month)

- Equipment: Camera gear, tools ($50-300/month)

Real Example: Carlos rented his spare bedroom on Airbnb 15 nights/month at $75/night = $1,125/month = $13,500/year in extra savings.

Consideration: Check local regulations and insurance requirements.

20. Maximize Credit Card Rewards (Earn $500-1,500 Annually)

Why it works: Strategic credit card use earns cash back or travel points without spending extra.

Forbes Advisor regularly updates rankings of the best cash-back credit cards to help you maximize rewards.

Best strategy:

- Use 2-3 cards for different categories

- Pay full balance monthly (avoid interest)

- Maximize category bonuses

Example setup:

- Groceries: 3% cash back card

- Gas: 3% cash back card

- Everything else: 2% cash back card

Real Example: The Park family spends $4,000/month on cards (paid in full):

- Groceries ($800): 3% = $24/month

- Gas ($200): 3% = $6/month

- Other ($3,000): 2% = $60/month

- Total: $90/month = $1,080/year in free money

Warning: Only use this strategy if you pay balances in full. Interest charges negate rewards.

📊 Plan Your Taxes to Save More

Understanding your tax situation helps you keep more of what you earn. Use these calculators to optimize your finances:

Part 5: Smart Shopping and Lifestyle Hacks

21. Buy Generic Brands (Save 30-40% on Groceries)

Why it works: Generic/store brands are often made in the same facilities as name brands but cost significantly less.

Best generic swaps:

- Medications (FDA-approved identical formulas)

- Pantry staples (flour, sugar, rice, pasta)

- Cleaning products

- Paper products

- Dairy products

Real Example: By switching to generic brands, the Thompson family reduced their $800 monthly grocery bill to $550, saving $250/month = $3,000/year with no quality difference.

Exceptions: Some items where brand matters (personal preference items, specific dietary needs).

22. Use Price Comparison Tools (Never Overpay Again)

Why it works: Prices vary dramatically between retailers. Comparison tools find the best deals instantly.

Essential tools:

- Honey: Automatic coupon codes + price tracking

- CamelCamelCamel: Amazon price history

- Google Shopping: Compare prices across retailers

- Rakuten: Cash back on purchases

- Slickdeals: Community-sourced deals

CNBC Select reviews the best price comparison tools and browser extensions to help you save money on every purchase.

Real Example: Before buying a $400 laptop, Maria used CamelCamelCamel and discovered the price dropped to $280 three weeks earlier. She set a price alert and bought it at $295 two weeks later, saving $105.

Pro Tip: Combine price comparison with cash-back apps for double savings.

23. Time Your Purchases (Buy When Prices Drop)

Why it works: Retailers follow predictable discount cycles. Strategic timing saves 30-70%.

Best times to buy:

- January: Fitness equipment, linens, winter clothes

- February: TVs (post-Super Bowl), winter sports gear

- May: Mattresses, appliances

- July: Furniture, summer clothes

- September: Cars (new models arriving)

- November: Electronics (Black Friday)

Real Example: Instead of buying a mattress in March, Jordan waited until Memorial Day sales in May and got a $1,200 mattress for $650 (46% off), saving $550.

Holiday shopping: Buy Christmas gifts in January clearance sales for next year.

24. DIY When Possible (Save on Services)

Why it works: Labor costs often exceed materials by 200-400%. Learning basic skills saves thousands.

High-impact DIY projects:

- Home maintenance: Painting, basic plumbing, lawn care

- Car maintenance: Oil changes, air filters, wiper blades

- Personal care: Haircuts, manicures, house cleaning

- Gifts: Homemade items vs. store-bought

Real Example: Instead of paying $80 for oil changes 4× yearly, Mike learned to do it himself (cost: $25 in materials). Annual savings: $220. Combined with other DIY tasks (lawn care, painting), he saved $2,400/year.

Resources: YouTube tutorials, library books, community workshops.

25. Practice Mindful Spending (The Most Powerful Habit)

Why it works: Conscious spending aligns purchases with values, eliminating waste on things that don't matter.

The mindful spending framework:

- Before buying, ask: "Does this align with my goals?"

- Calculate in hours worked: "$100 purchase = 5 hours of work. Worth it?"

- Identify needs vs. wants: Be honest about necessity

- Consider opportunity cost: "This $50 could be $500 in 10 years invested"

Real Example: After adopting mindful spending, Rachel realized she spent $200/month on clothes she rarely wore. She redirected that money to her investment account. Over 5 years at 8% return: $14,680 instead of a closet full of forgotten clothes.

Philosophy: Spend lavishly on what you love, cut mercilessly on what you don't.

🔥 Viral Money-Saving Challenges (TikTok-Approved!)

Join millions of people worldwide who are using these trending savings challenges to build wealth fast. Pick one challenge and start today!

Creating Your Personalized Money-Saving Plan

Step 1: Assess Your Current Situation

- Calculate monthly income and expenses

- Identify your top 5 expense categories

- Determine realistic savings goal

Use our Top 10 Financial Calculators to assess your complete financial picture and create a data-driven savings plan.

Step 2: Choose Your Top 5 Strategies

Select strategies from this guide that fit your lifestyle:

- 2 expense-cutting strategies

- 2 income-increasing strategies

- 1 automation/system strategy

Step 3: Implement Gradually

- Week 1: Set up tracking and automation

- Week 2-3: Implement first 2 strategies

- Week 4: Add remaining strategies

- Month 2+: Optimize and adjust

Step 4: Track Progress

- Review savings weekly

- Celebrate milestones

- Adjust strategies as needed

Frequently Asked Questions (FAQs)

How can I save money fast with a low income?

Even on a tight budget, you can save money quickly by focusing on high-impact strategies:

- Start micro-saving: Save just $5-10 per week ($260-520/year)

- Cut one major expense: Cancel unused subscriptions or negotiate bills (save $50-100/month)

- Increase income: Start a side hustle earning even $200/month extra

- Use free resources: Libraries, community programs, and free entertainment

- Automate small amounts: Even $25/paycheck adds up to $650/year

Real example: Maria earned $2,200/month and felt she couldn't save. She canceled $45 in subscriptions, started freelancing 5 hours/week ($200/month), and automated $50/paycheck. Result: $395/month saved = $4,740/year without major lifestyle changes.

The key is starting small and being consistent. Every dollar saved compounds over time.

What is the 50/30/20 rule for saving money?

The 50/30/20 rule is a simple budgeting framework that divides your after-tax income into three categories:

- 50% for Needs: Essential expenses like rent/mortgage, utilities, groceries, insurance, minimum debt payments, and transportation

- 30% for Wants: Non-essential spending like dining out, entertainment, hobbies, subscriptions, and shopping

- 20% for Savings: Emergency fund, retirement contributions, investments, and extra debt payments

Example on $4,000 monthly income:

- Needs: $2,000 (housing $1,200, utilities $150, groceries $400, insurance $150, transportation $100)

- Wants: $1,200 (dining out $300, entertainment $200, hobbies $200, subscriptions $100, shopping $400)

- Savings: $800 (emergency fund $300, retirement $400, extra debt payment $100)

For aggressive savers: Adjust to 50/20/30 or 50/10/40 to accelerate wealth building. The rule is flexible based on your goals and life stage.

How much money should I save each month?

The amount you should save depends on your income, expenses, and financial goals, but here are general guidelines:

Minimum recommendations:

- Emergency fund phase: 10-20% of income until you have 3-6 months of expenses saved

- Debt payoff phase: 15-20% toward debt elimination

- Wealth building phase: 20-30% for investments and long-term goals

Use our Paycheck Calculator to determine your exact take-home pay and calculate how much you can realistically save each month.

By income level:

- $2,000/month income: Save $200-400 (10-20%)

- $4,000/month income: Save $600-1,200 (15-30%)

- $6,000/month income: Save $1,200-1,800 (20-30%)

Start with what you can afford, even if it's just $25/week, and increase as your income grows.

What are the best apps for saving money automatically?

The best money-saving apps in 2025 automate savings, track spending, and help you reach financial goals faster:

Best Overall Savings Apps:

- Digit - Analyzes spending patterns and automatically saves small amounts you won't miss. Average users save $2,500/year.

- Qapital - Rule-based savings (round-ups, goal-based triggers). Great for visual goal tracking.

- Acorns - Rounds up purchases to nearest dollar and invests the difference.

Best Budgeting Apps:

- YNAB (You Need A Budget) - Zero-based budgeting system. Users report saving $600 in the first two months.

- Mint - Free comprehensive budgeting, bill tracking, and credit score monitoring.

- PocketGuard - Shows how much you can safely spend after bills and savings goals.

Real example: Jason used three apps simultaneously: Digit (automated $150/month), Truebill (canceled $45/month subscriptions), Rakuten (earned $25/month cash back). Total: $220/month = $2,640/year saved automatically

How can I save $10,000 in a year?

Saving $10,000 in one year requires saving approximately $833/month or $192/week. Here's a realistic action plan:

Strategy 1: Expense Reduction ($400/month)

- Cancel subscriptions: $100/month

- Meal planning and packed lunches: $200/month

- Negotiate bills (internet, insurance): $100/month

Strategy 2: Income Increase ($433/month)

- Side hustle 10 hours/week at $25/hour: $1,000/month (save $433)

Total: $833/month = $10,000/year

Real example: The Martinez family saved $10,000 in 12 months by canceling subscriptions ($120/month), meal planning ($250/month), negotiating bills ($80/month), and starting a freelance side hustle ($400/month saved). Result: $10,200 saved in 12 months

What are the biggest money-wasting habits to avoid?

The most common money-wasting habits that prevent people from building wealth:

- Paying for unused subscriptions ($200-500/year) - Average household has 4+ forgotten subscriptions. Solution: Audit monthly, use apps like Truebill

- Impulse buying ($1,000-3,000/year) - Emotional purchases that don't align with goals. Solution: 30-day rule for non-essential purchases

- Paying credit card interest ($1,000-5,000/year) - Average American pays $1,155/year in credit card interest. Solution: Pay balances in full, use balance transfer cards

- Not negotiating bills ($500-1,500/year) - Accepting default rates on insurance, internet, phone. Solution: Call annually to negotiate or switch providers

- Daily coffee shop visits ($1,500-2,000/year) - $5 daily coffee = $1,825/year. Solution: Brew at home, limit to 2× weekly treat

- Food waste ($1,500-2,000/year) - Average family throws away 30% of groceries. Solution: Meal planning, proper storage, use leftovers

- Buying new cars ($5,000-10,000 lost to depreciation) - New cars lose 20-30% value in year one. Solution: Buy 3-5 year old certified pre-owned

- Not using employer 401(k) match (thousands in free money) - 25% of employees don't contribute enough to get full match. Solution: Contribute at least enough to get full match

- Paying ATM fees ($200-300/year) - $3-5 per transaction adds up quickly. Solution: Use your bank's ATMs or get cash back at stores

- Lifestyle inflation (consuming all raises) - Spending increases match income increases. Solution: Save 50% of every raise

Real example: Before fixing these habits, Tom wasted:

- Unused gym membership: $540/year

- Credit card interest: $1,200/year

- Daily coffee: $1,800/year

- Impulse purchases: $2,000/year

- Total waste: $5,540/year

After implementing solutions, he redirected this money to savings and investments, building a $30,000 emergency fund in 5 years.

How do I start an emergency fund with no money?

Starting an emergency fund from zero is challenging but achievable with these steps:

Phase 1: Starter Emergency Fund ($1,000)

Week 1-2: Find immediate money

- Sell unused items: $200-500

- Return unused purchases: $50-100

- Cancel one subscription: $10-50/month freed up

Week 3-4: Redirect existing spending

- Pack lunches for 2 weeks: $100 saved

- Skip coffee shops: $50 saved

- No dining out: $100 saved

Month 2-3: Micro-savings

- Save $10/week: $40/month

- Round-up savings app: $30/month

- Side hustle 5 hours: $100/month

Timeline: $1,000 in 3-4 months

Phase 2: Full Emergency Fund (3-6 months expenses)

Once you have $1,000, continue building:

- Automate $200-500/month to high-yield savings

- Add all windfalls (tax refunds, bonuses)

- Increase savings by 1% monthly

Real example: Starting with $0, Jennifer:

- Month 1: Sold items ($300), canceled subscriptions ($40/month)

- Month 2: Saved $200 from packed lunches and no dining out

- Month 3: Started side hustle earning $400/month (saved $300)

- Month 4: Reached $1,000 emergency fund

- Months 5-16: Saved $500/month to reach $6,000 full emergency fund

Motivation tips:

- Keep emergency fund in separate high-yield savings account

- Name the account "Do Not Touch - Emergencies Only"

- Track progress visually with a chart

- Celebrate milestones ($250, $500, $1,000)

The key is starting with any amount, even $5/week, and building the habit of consistent saving.

Should I save money or pay off debt first?

This is one of the most common financial dilemmas. The answer depends on your specific situation:

The Balanced Approach (Recommended for Most):

Step 1: Save $1,000 starter emergency fund first - Prevents new debt when emergencies arise and provides psychological security to focus on debt

Step 2: Pay off high-interest debt (>7% APR) - Credit cards (15-25% APR), Personal loans (10-20% APR), Payday loans (400%+ APR)

Step 3: Build full emergency fund (3-6 months expenses) - While making minimum payments on remaining debt

Step 4: Pay off moderate-interest debt (4-7% APR) - Car loans, Student loans - While continuing to save 10-15%

Step 5: Invest while paying low-interest debt (<4% APR) - Mortgages, Federal student loans - Investment returns typically exceed these rates

The Math:

High-interest debt example:

- $10,000 credit card at 20% APR costs $2,000/year in interest

- Paying this off is like earning a guaranteed 20% return

- Priority: Pay off immediately

Low-interest debt example:

- $10,000 car loan at 3% APR costs $300/year in interest

- Investing $10,000 at 8% average return earns $800/year

- Priority: Invest while making regular payments

Real example: Sarah had:

- $15,000 credit card debt at 22% APR

- $25,000 student loans at 4% APR

- $0 emergency fund

Her strategy:

- Saved $1,000 emergency fund (2 months)

- Attacked credit card debt aggressively ($1,000/month for 15 months)

- Built 6-month emergency fund ($12,000 over 12 months)

- Now paying student loans normally while investing 15% of income

Result: After 30 months, she had no credit card debt, $12,000 emergency fund, and started building wealth through investments.

The psychological factor: Some people need the "win" of paying off debt for motivation, even if mathematically saving makes more sense. Mental health matters in financial decisions.

What's the difference between saving and investing?

Saving and investing are both crucial for financial health but serve different purposes:

Saving:

Definition: Setting aside money in safe, liquid accounts for short-term goals and emergencies.

Characteristics:

- Low risk (FDIC insured up to $250,000)

- High liquidity (access money anytime)

- Low returns (4-5% in high-yield savings in 2025)

- No loss of principal

Best for:

- Emergency fund (3-6 months expenses)

- Short-term goals (<3 years): vacation, car down payment

- Money you can't afford to lose

Where to save: High-yield savings accounts, Money market accounts, Certificates of Deposit (CDs)

Example: $10,000 in high-yield savings at 4.5% APY earns $450/year with zero risk.

Investing:

Definition: Putting money into assets that have potential to grow significantly over time, with some risk of loss.

Characteristics:

- Higher risk (value fluctuates)

- Lower liquidity (may take days to access, penalties for early withdrawal)

- Higher returns (8-10% average annually for stock market)

- Potential for loss of principal

Best for:

- Long-term goals (5+ years): retirement, house down payment, wealth building

- Money you won't need soon

- Building wealth that outpaces inflation

Where to invest: Stock market (index funds, ETFs), Retirement accounts (401k, IRA), Real estate, Bonds

Example: $10,000 invested in S&P 500 index fund averaging 10% annually becomes $25,937 in 10 years (vs. $15,530 in savings at 4.5%).

Real example: Michael, age 30, earning $60,000/year:

Saving (30% of income = $1,500/month):

- Emergency fund: $15,000 in high-yield savings (complete)

- House down payment fund: $500/month (goal: $40,000 in 5 years)

Investing (20% of income = $1,000/month):

- 401(k): $600/month (with employer match = $750/month)

- Roth IRA: $400/month

Result after 10 years:

- Emergency fund: $15,000 (stable)

- House fund: $40,000 (saved)

- Retirement accounts: $150,000+ (invested and grown)

Key takeaway: Save for security and short-term goals. Invest for long-term wealth building. You need both for complete financial health.

How can I save money on groceries without sacrificing quality?

You can cut grocery costs by 30-50% without eating poorly by using these strategic approaches:

Strategy 1: Smart Shopping Habits

Plan before you shop:

- Create weekly meal plan based on sales

- Make detailed shopping list

- Never shop hungry (impulse purchases increase 30%)

- Shop alone when possible (kids/partners add $20-50 to cart)

Shop strategically:

- Compare unit prices (price per ounce), not package prices

- Buy store brands (same quality, 30-40% cheaper)

- Shop seasonal produce (50-70% cheaper)

- Use cash-back apps (Ibotta, Fetch Rewards earn $10-30/month)

Real example: The Johnson family reduced groceries from $900 to $550/month:

- Meal planning: Saved $150/month (less waste, fewer emergency takeout orders)

- Store brands: Saved $120/month

- Seasonal produce: Saved $50/month

- Cash-back apps: Earned $30/month

- Total savings: $350/month = $4,200/year

Strategy 2: Buy Smart, Not Cheap

Buy in bulk (only what you'll use): Rice, pasta, beans, oats, Frozen vegetables (as nutritious as fresh, 50% cheaper), Meat on sale (freeze in portions)

Best value proteins:

- Eggs: $0.20-0.30 per egg (6g protein)

- Chicken thighs: $1.50-2/lb (vs. $4-5 for breasts)

- Canned tuna: $1/can (20g protein)

- Dried beans: $0.15/serving (15g protein)

- Ground turkey: $3-4/lb

Strategy 3: Reduce Waste

Average family wastes $1,500/year in food. Use "first in, first out" method, freeze before it spoils, and use leftovers creatively.

Real example: Maria spent $700/month on groceries but threw away $150/month in spoiled food. After implementing meal prep Sundays, freezing extras immediately, and "use it up" meals on Fridays, waste reduced to $20/month, saving $130/month = $1,560/year.

Action plan this week: Inventory what you have, plan 7 dinners using sales and what you own, make detailed shopping list, download one cash-back app, and shop with list only. Most families save $100-300 in the first month alone.

Ready to Start Saving Money Today?

Use our free financial calculators to create your personalized savings plan and track your progress: